Balancing collateral optimization and regulatory compliance front to back through “Holistic Collateral Architecture”

July 28, 2017

Collateral Business Transformation

Financial institutions today are increasingly evaluating how best to manage their collateral needs in the face of dual challenges – how to adapt their business and operational structures to become more efficient and how to respond to and comply with ongoing demands around changing regulatory requirements. These issues resemble a seemingly difficult task, like transferring passengers from one train to another, while both trains are in motion. Firms that approach front office transformation challenges, decoupled from regulatory and compliance challenge, will miss opportunities to solve larger systemic issues in a strategic and integrated fashion. We strongly believe that Technology strategy and architecture can play a critical role as firms evolve to meet these challenges. This article looks at how businesses can strategically address their collateral and liquidity management operations and regulatory needs by adopting a more holistic integration approach that takes into account their organizational complexity, unique business requirements and their compliance mandates. Firms that get this strategy right will establish a competitive advantage and maximize limited budgets by significantly enhancing their front office capabilities, while also meeting regulatory requirements.

Managing Business Transformations and Regulatory Challenges Simultaneously

Global regulations such as Dodd-Frank, Basel, MIFID and EMIR are demanding significant changes to securities finance and derivatives businesses which are primary drivers of collateral flow. An organization’s overall portfolio mix dictates the cost of doing business, and having an integrated view of the complete liquidity situation is critical and can’t be done in isolation. These regulatory and economic forces are driving firms to integrate their collateral businesses that traditionally operated as silos.

At the same time, new global regulations are mandating that firms implement specific capabilities and requirements that are often quite broad, impacting many aspects of collateral and liquidity management capabilities. Consequently, these requirements are quite onerous to accomplish especially because they need to be implemented at an enterprise level.

What is Required for Front Office Optimization?

Typically, financial business units were structured and incentivized to take a highly localized approach to addressing the collateral requirements for their specific business lines. This historical constraint was driven by a need for domain expertise and reinforced by budgeting protocols and performance expectations that were more closely aligned with local returns on capital, revenue and income. In the current environment, making decisions within a single function misses the opportunity to achieve broader benefits to drive valuable optimization across an enterprise. The outlying boxes in the diagram below illustrate the standard, localized organizations that exist in most firms today, where individual business units make collateral decisions without consideration of their sister business’ needs.

Firms that move beyond the silo approach and evaluate and prioritize collateral and liquidity requirements in a more integrated fashion across all their collateral management processes are better positioned to ensure the optimal allocation of capital and costs, realize efficiency gains and enhanced profitability. Some organizations are doing this by establishing collateral optimization units that have a mandate to implement technology and organizational changes across multiple businesses on a front-to-back basis. Potential areas that organizations are evaluating include maximizing stress liquidity, streamlining operational processing, reducing the balance sheet by retaining high-quality HQLA and improving the firm’s funding profile by reducing liquidity buffers against bad trades for non-LCR compliant transactions.

What is Required for Regulatory Compliance?

While many front office businesses typically focus on creating optimal technology architecture to improve financial return metrics, there are specific regulatory-focused technology enhancements that additionally need to be implemented. In most cases, these regulatory requirements are implemented by compliance and/or operations areas potentially away from the front office functions. This is a big challenge as these requirements are at the firm level and most firms don’t have a coordinated collateral architecture in the front. In particular, Recovery and Resolution Planning (RRP) requirements, Qualified Financial Contracts (QFC) specifications, Secured Financing Transaction Reporting (SFTR) are few examples that have pressing requirements and deadlines in the near future.

These regulations are creating significant demands on large institutions’ business and technology architecture:

- Track and report on firm and counterparty collateral by jurisdiction (RRP – SR 14-1)

- Track sources and uses of collateral at a security level across legal entities (RRP – 2017 guidance)

- Conduct scenario-planning to simulate market stresses, such as a ratings downgrade or other environmental changes, that estimate impact on collateral and liquidity position in stress scenarios on a periodic basis (RRP – SR 14-1 and 2017 guidance)

- Deliver daily information on their collateral and liquidity positions. Specific QFC (Qualified Financial Contract) reports will cover position-level, counterparty-level exposures, legal agreements and detailed collateral information. (QFC Specifications)

- Report on all Securities Financing transactions (SFTR – Europe)

To fully meet these compliance deadlines within the next 12 to 24 months, most firms do not have the luxury of adopting a strategic approach to re-engineer their business and technology architecture and have been forced to take tactical steps to ensure compliance. However, it is likely that achieving compliance in a short timeframe will create huge business and operational overhead costs, as one-off solutions may not be tightly integrated and may require additional manual work and reconciliations over time. The ongoing need for changes to front office business processes will have an impact on compliance solutions – potentially causing firms to significantly increase the operational overhead of supporting these businesses.

This can lead to a rather unfortunate outcome, in that costs for collateral businesses can significantly increase, despite working hard to drive cost & capital efficiencies.

A BETTER APPROACH – HOLISTIC ARCHITECTURE

Firms that choose to tackle these operational and regulatory challenges head-on and invest to create and establish an integrated collateral architecture across business lines will have a significant competitive advantage. In a dynamic marketplace where business needs and regulatory requirements are constantly evolving, a component-based architecture can be an effective approach. This allows seemingly complex processes to be managed through careful consideration of the distinct business and technology architecture elements of each stakeholder to achieve the appropriate balance for their strategy in an effective manner.

Key Components of Holistic Collateral Architecture

Here are some important drivers to consider in your planning:

- Real-time inventory management capabilities across business lines that can be leveraged by both the front and back-office. This is a critical component of the strategic architecture, with the key requirement of knowing firm, counterparty and client collateral by jurisdiction.

- QFC trades repository that is integrated across all Secured Financing Transactions as well as derivatives trades that can be linked with positions, margin calls and collateral postings.

- Harmonized collateral schedules / legal agreements repository across ISDA, CSAs, (G)MRAs, (G)MSLAs, triparty, etc.

- Enabling collateral traceability across legal entities with the ability to produce sources and uses of collateral will ensure regulatory compliance, as well as the ability to implement appropriate transfer pricing rules to drive business incentives in the right places.

- Utilizing optimization algorithms with targeted analytics can maximize a variety of different business opportunities and most importantly recommend actions through seamless operational straight through processing.

This transition can be difficult for firms as it will need to cut across business and functional silos and it can have significant people and organizational hurdles along with technology challenges. One key point is that these changes don’t need to happen all at the same time and firms can prioritize the approach in a phased manner in line with their pain points and priorities as long as leadership is behind the vision of the holistic architecture. Many firms have started this journey and those who can make demonstrable progress in this evolution will have a significant competitive advantage in the new era.

How Transcend can help…

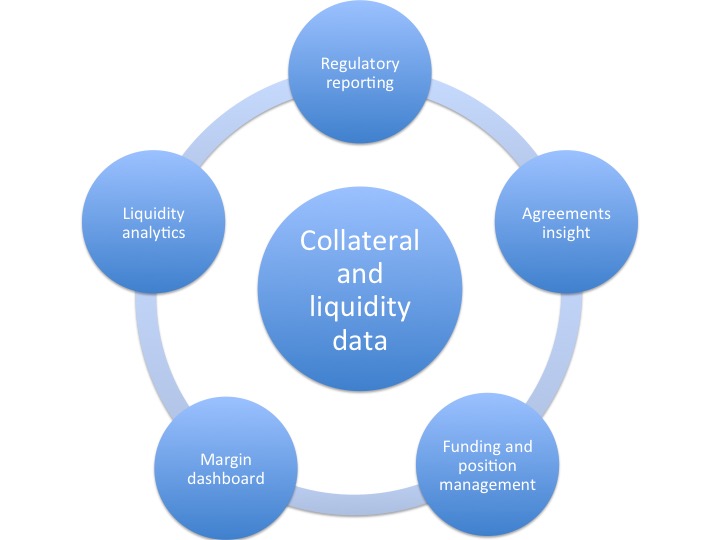

We have leveraged decades of Wall Street experience to develop strategic collateral and liquidity solutions for the largest, most sophisticated banks and financial institutions. Recognizing the unique requirements and opportunities financial organizations have to optimize liquidity and collateral across business units, we have developed solutions that address the need for Collateral Optimization, Agreements Insights, a Margin Dashboard, Real-Time Inventory and Position Management and Liquidity Analytics. Separately or in combination, these tools will help your firm take a more strategic approach to optimizing the best assets across your entire portfolio and businesses to maximize your profitability.

To discuss your firm’s requirements, contact us.

References:

- January 2013: Basel III: The Liquidity Coverage Ratio and liquidity risk monitoring tools

- October 2013: Basel Committee on Banking Supervision Working Paper No. 24 – Liquidity stress testing: a survey of theory, empirics and current industry and supervisory practices

- January 24, 2014: Federal Reserve Bank (FRB) released Supervision and Regulation letter (SR letter 14-1) entitled “Heightened Supervisory Expectations for Certain Bank Holding Companies,” and Attachment Principles and Practices for Recovery and Resolution Preparedness

- SR letter 12-1 entitled “Consolidated Supervision Framework for Large Financial Institutions”

- SR 14-1: Additional Guidance from Federal Deposit Insurance Corporation, Board of Governors of the Federal Reserve System entitled “Guidance for 2017 §165(d) Annual Resolution Plan Submissions by Domestic Covered Companies that Submitted Resolution Plans in July 2015”

This article was originally published in Securities Lending Times.

{kind=link}

{kind=link}