ESG Collateral Management and Trading: Preparing Today for Tomorrow’s Requirements

- Oct 14, 2021

- Blog Capital Markets Collateral Management ESG

Members of the collateral ecosystem are beginning to explore how best to serve the needs of investors with ESG funds. Some institutions are starting to manually support ESG in trading and collateral processes such as green bond baskets in repo or excluding securities in the agent lending market. As beneficial owners provide stricter collateral guidelines in line with their ESG policies, agent lenders and the broader collateralized markets must consider how to best incorporate ESG criteria into collateral management workflows. A guest post from Transcend.

Framing the ESG conversation

ESG requirements broadly impact the financial services value chain from determining which assets investors hold in their portfolios, to what assets and at what rates those portfolios will be financed, to downstream collateral management processes that support securities lending, collateral pledging, and asset servicing.

ESG investing receives the most attention from investors, regulators and the media. ESG-branded funds are seeing increased capital flows and continue to attract new investors. As a result, regulators are working to govern this expanding market and are publishing additional regulatory guidelines such as Europe’s Sustainable Finance Disclosure Regulation (SFDR). An increased regulatory focus includes standardizing ESG financial disclosures to ensure investors utilize a common framework for reporting. The media often conflates ESG concerns across greater transparency, the practice of greenwashing of legacy assets and the use of appropriate metrics across the industry.

Beyond ESG investing, early adopters are beginning to extend the ESG conversation to securities financing across securities lending, repo and OTC derivatives. Recent repo transactions associated with ESG goals have evidenced the ability to tie the economics of the trade to ESG performance, and green bond baskets can be financed at preferential terms under what is sometimes referred to as green repo. As an example, Deutsche Bank structured a $300 million deal with Turkey’s Akbank where the repo interest rate was based on Akbank’s gender balance, electricity sourcing and no greenfield coal power plant loan origination. This is the beginning of ESG financing: in a few short years, there may well be a new industry standard that defines these ESG repo transactions with a large community of funders.

The acceleration of ESG investing and the emerging ESG financing market is starting to trickle down to collateral management processes. These processes have long governed how securities are lent to counterparties for short covering, proxy voting and the use of collateral to meet margin requirements across products. For example, as more investors express the desire to reflect their ESG goals in proxy votes, recall mechanisms have been tightened to support specific investor requirements.

However, despite the growing interest in integrating ESG into securities financing, securities lenders, even those with ESG funds, do not uniformly report that ESG is a factor in their securities lending programs today. Recent research from Finadium revealed that 53% of large asset managers say that ESG is a consideration in proxy voting linked to securities lending, but only a handful have fully integrated ESG through the lending and collateral process. This is expected to change as beneficial owners require firms to implement their ESG requirements with the same automation as they do today with credit rating and concentration limit requirements. Supporting these clients means tying individual securities to relevant acceptance criteria. Transactions like the Deutsche Bank and Akbank arrangement will need to be codified across hundreds of thousands, if not millions, of equity and fixed income securities.

The future assimilation of ESG in collateral management necessitates flexible technology architectures that can support today’s processes yet scale to meet future requirements across multiple counterparties that have implemented their ESG frameworks differently.

Exclusion lists are only the beginning

The current mechanism to ensure that collateral is in line with ESG expectations is to create exclusion lists that specify certain assets that do not meet ESG criteria. This could include oil and gas stocks or bonds linked to mining companies. Given the opportunity for customization, the exclusion list methodology allows counterparties the flexibility to implement their own internal ESG policies. While this may not tie directly to a recognized ESG scoring mechanism or metric, it enables firms to support varying client ESG needs across counterparties. The model is not scalable however: short-term requirements are limited, but the exclusion list methodology requires manual setup and ongoing maintenance, which is unrealistic for future growth in a market with ESG standardization.

Exclusion lists also impact cash managers in collateral. Some cash funds have declared themselves to be ESG-compliant. A government money market fund, for example, may be considered ESG-friendly by default if US Treasury bills or other developed country government bonds are not seen as going against ESG principles. As a result, if a cash fund’s ESG status is based on excluding certain types of transactions altogether rather than setting up exclusion lists on a per-security basis, the exclusion list methodology will be insufficient.

A scalable ESG collateral process is critical but not easy

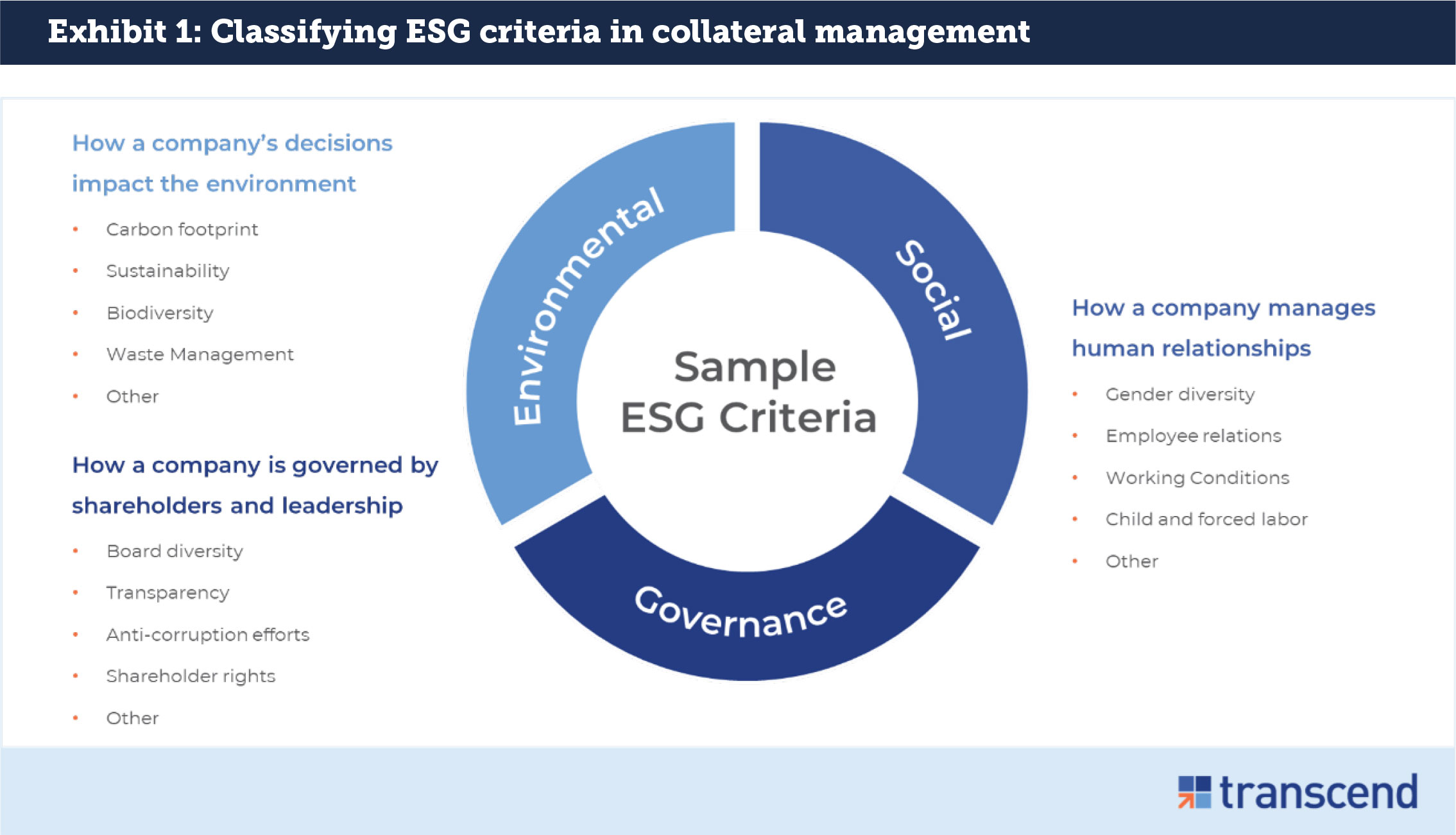

Given the limitations of exclusion lists and growing popularity of ESG metrics and scoring, the future of the ESG collateral management ecosystem must be able to integrate recognized, trusted, and readily available ESG data. This integration will allow firms to evaluate each asset against granular counterparty criteria to determine whether it is ESG-eligible. The process requires the asset to be tagged with metadata that indicates granular ESG metrics across the E, S, and G components, including sub-criteria such as the percentage of women on the board or carbon emissions/intensity (see Exhibit 1).

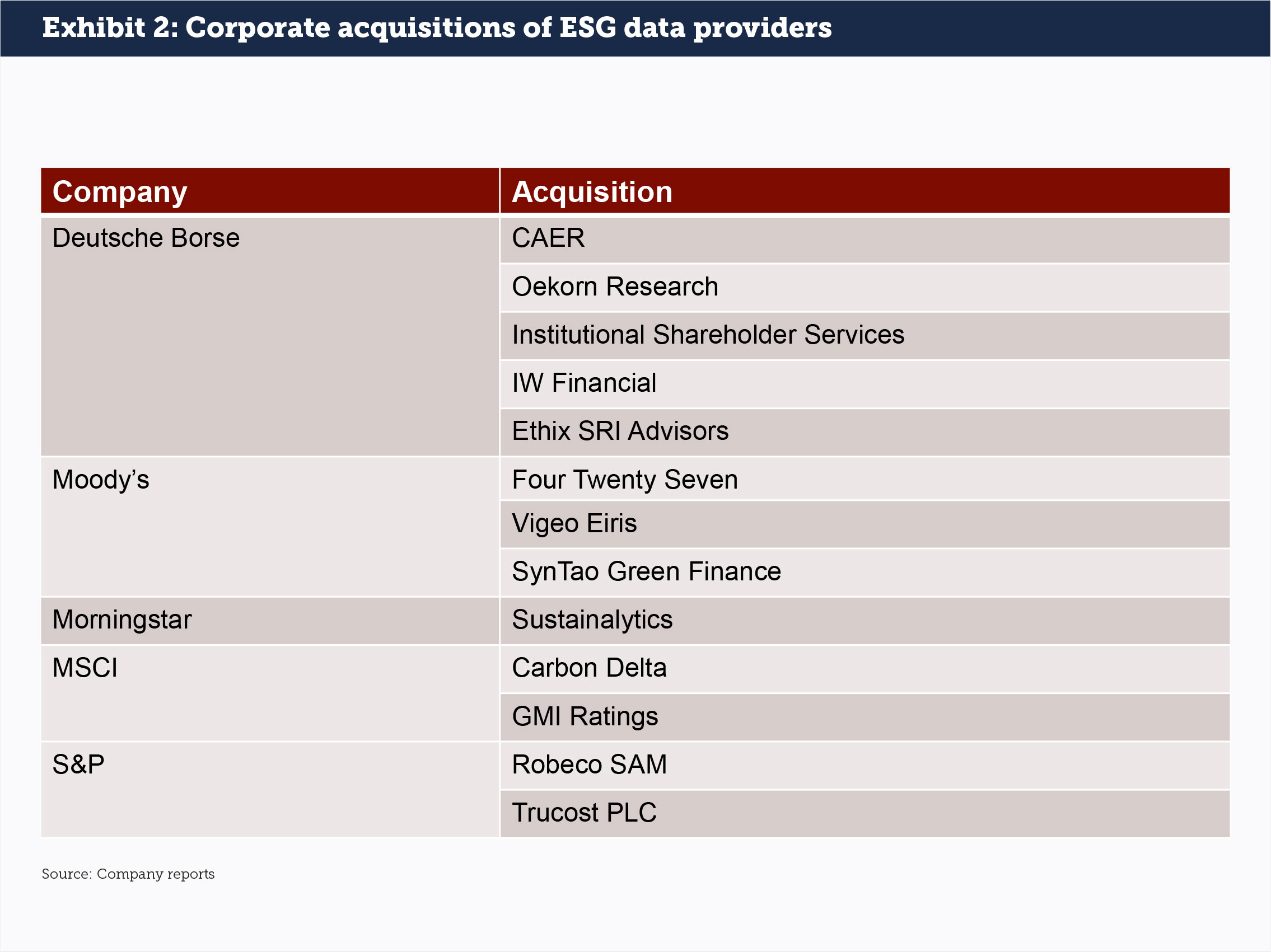

Recent studies from the United Nations Environment Programme Finance Initiative, the Network for Greening the Financial System and others note that while methodologies for assessing climate risk are exploding, they all rely on data that may or may not be readily available. While large data providers and startups alike are building out ESG data frameworks either directly or via acquisition, none are at the point where they cover all asset classes and metrics (see Exhibit 2). Nevertheless, the accessibility of ESG data will continue to grow as time progresses.

Without clear reporting standards from issuers, standardization on which metrics should be trusted and reliable data providers, incorporating ESG metadata in a scalable fashion will be a major challenge. A holistic approach provides the granularity that firms need to not only support specialized exclusion lists from firms who use internal criteria but also allow collateral givers and receivers to use established criteria to test whether collateral is allowed. While today it may be possible to manually manage new collateral requirements and utilize legacy collateral technology, even modest growth in ESG requirements from beneficial owners will outpace current capabilities. Soon firms will need to integrate ESG data to ensure they can meet ESG expectations while continuing to support collateral optimization and straight-through-processing efforts.

The pivotal role of inventory management

Some market participants already tag metadata such as a security’s origination, whether it can be rehypothecated or not, and its credit rating. However, adding further metadata, ESG included, requires a higher degree of sophistication. To successfully fold ESG capabilities into collateral trading, funding and management workflows, market participants need an inventory management platform that can support ESG data in varying formats. Otherwise, they will need to outsource the process entirely to service providers such as tri-party agents.

The collateral industry must evolve to meet rising ESG challenges. While today the industry sees bespoke requirements from particular counterparties, soon firms across the board will transition ESG collateral conversations from theory to action. First, collateral receivers like agent lenders and cash providers will require validated and actionable ESG data on inventory holdings. Then, collateral givers and risk managers will follow. These are the levers that will force fast movement for ESG collateral management.

This article was originally published on Securities Finance Monitor.