Collateral management has broadened far past simple margin processing; collateral now impacts a majority of financial market activity from determining critical capital calculations to impacting customer experience to driving strategic investment decisions. In this article, we identify the top five trends in collateral management for 2018 and highlight important areas to watch going forward.

The holistic theme driving forward collateral management is its central role in financial markets. Collateral has grown so broad as to make even its name confusing: where collateral can refer to a specific asset, the implications of collateral today can reach through reporting, risk, liquidity, pricing, infrastructure and relationship management. The opportunities for collateral professionals have likewise expanded, and non-collateral roles must now have an understanding of collateral to deliver their core obligations to internal and external clients.

We see a common theme running through five areas to watch in collateral management in the coming year: the application of smarter data and intelligence to drive core business objectives. Many firms have digested the basics of collateral optimization and are now ready to incorporate a broader set of parameters and even a new definition of what optimization means. Likewise, technology investments in collateral are starting to tie into broader innovation projects at larger firms; this will unlock new value-added opportunities for both internal and external facing technology applications.

Here are our top five trends for collateral management in 2018:

#5 Technology Investments

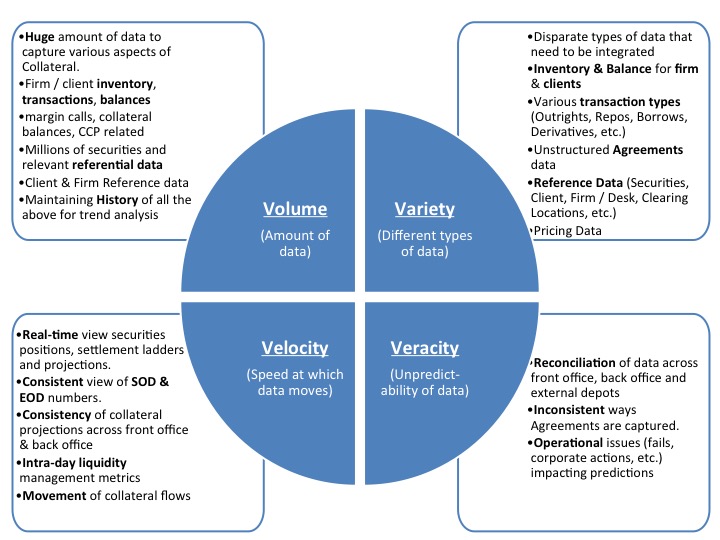

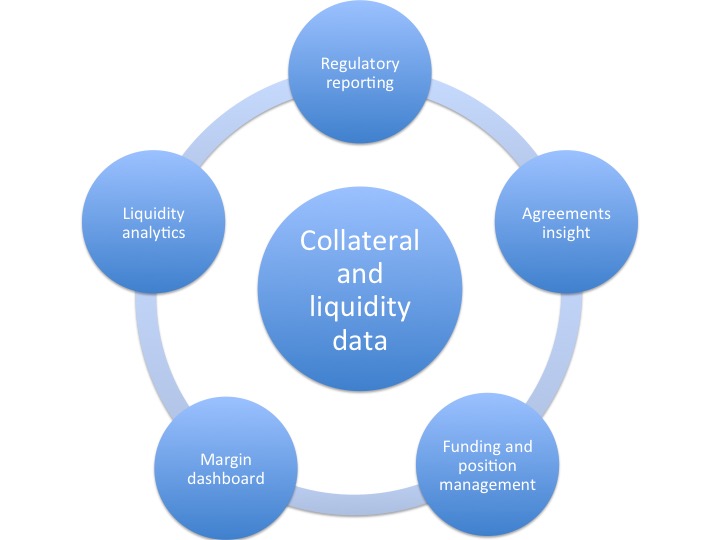

The investment cycle in collateral-related technology applications continues to grow at a rapid pace. Collateral management budget discussions are moving from the back office to the top of the house. And partly as a result, the definition of the category is also changing. Collateral management should no longer be seen as strictly the actions of moving margin for specified products, but rather is part of a complex ecosystem of collateral, liquidity, balance sheet management and analytics. The usual, first order investment targets of these budgets are internally focused, including better reporting, inventory management and data aggregation. The second derivative benefit of a more robust data infrastructure focuses on externally facing trading applications, including tools for traders and client intelligence utilities that provide real-time information and pricing for the benefit of all parties. This new category does not yet have a simple name, one could think of it as a “recommendation system” but regardless of name, this has become a major driver of forward-looking bank technology efforts and efficiency drives.

As large financial services firms capture the benefits of their current round of investments, they will increasingly turn towards integrating core innovations in artificial intelligence, Robotics Process Automation and other existing technologies into their collateral-related investments. This will unlock a large new wave of opportunity for how business is conducted and what information can be captured, analyzed, then automated, for a range of client facing, business line, internal management and reporting applications.

#4 Regulatory reporting

Despite being 10 years since the bottom of the great recession, regulatory reporting requirements for banks and asset managers continue to evolve. Largely irrespective of jurisdiction, the core problem facing these firms is aggregating and linking data together for reporting automation. Due to strict timeframes and complex requirements, firms historically relied on a pre-existing mosaic of technology and human resources to satisfy regulatory reporting needs. However, these tactical solutions made scale, efficiency and responsiveness to new rules difficult. The challenge of regulatory reporting is a puzzle that, once solved, appears obvious. But the process of solving the puzzle can create substantial challenges.

Looking at one regulation alone misses the transformative opportunity of strategic data management across the organization. Whether it is SFTR, MiFID II, Recovery & Resolution Planning requirements of SR-14/17 or Qualified Financial Contracts (QFCs), the latest initiative du jour should be a kick off for a broader rethink about data utilization. Wherever a firm starts, the end result must be a robust data infrastructure that can aggregate and link information at the most granular level. At a high level, firms will need to develop the capability to link all positions and trading data with agreements that govern these positions, collateral that is posted on the agreements, any guarantees that may be applied and any other constraints that need to be considered. Additionally, it has to be able to format and produce the needed information on demand. Achieving this goal will take meaningful work but will make organizations not only more efficient but also more future proof.

#3 Transfer pricing

As firms try to optimize collateral across the enterprise, it is critical that they develop reasonably sophisticated transfer pricing mechanisms to ensure appropriate cost allocations as well as sufficient transparency to promote best incentives in the organization. Many sell-side firms have highly granular models with visibility into secured and unsecured funding, XVA, balance sheet and capital costs. And in varying fashion these firms allocate some or all of these costs internally. But many challenges remain, including: how should all these costs be directly charged to the trader or desk doing the trade; and what is the right balance of allocating actual costs versus incentivizing business behavior that maximally benefits the client franchise overall. As we know, client business profiles change through time as do funding and capital constraints. There may be a conscious decision to do some business that may not make money in support of other areas that are highly profitable. Transfer pricing is evolving from a bespoke, business aligned process to a dynamic, enterprise tool. The effort to enhance transfer pricing business models continues to be refined and expanded.

Firms that embrace the next iteration of transfer pricing will achieve a more scalable, efficient and responsive balance sheet. This will include capturing both secured and unsecured funding costs, plus firm-wide and business specific liquidity and capital costs. Accurately identifying the range of costs can properly incentivize business behaviors beyond simply the cost of an asset in the collateral market. Ultimately, transfer pricing can be a tool to drive strategic balance sheet management objectives across the firm.

Functionally, implementing transfer pricing requires access to substantial data on existing balance sheet costs, inventory management and liquidity costs that firms must consider. Much like collateral optimization, the building block of a robust transfer pricing methodology is data. Accurate information on transfer pricing can then flow back into trading and business decisions to be truly effective.

#2 Collateral control and optimization

Optimization is evolving well beyond an operations driven process of finding opportunity within a business to an enterprise wide approach at pre-trade, trade and post-trade levels. Pre-trade, “what-if” analyses that will inform a trader if a proposed transaction is cost accretive or reducing to the franchise is important, but this requires an analytics tool that can comprehend the impact to the firm’s economic ecosystem. At the point of trade, identifying demands and sources of collateral across the entire enterprise extends to knowing where inventories are across business lines, margin centers, legal entities and regions. It also means understanding the operational nuances and legal constraints governing those demands across global tri-parties, CCPs, derivative margin centers and securities finance requirements.

In a simple example, collateral posted on one day may not be the best to post a week later; if posted collateral becomes scarce in the securities financing market and can be profitably lent out, it may be unwise to provide it as margin. A holistic post-trade analysis, complete with updated repo or securities lending spreads, can tell a trader about missed opportunities, leading to a new form of Transaction Cost Analytics for collateralized trading markets.

#1 Integration of derivatives & securities finance (fixed income and equities)

The need for taking a holistic approach to collateral management has led the industry toward significant business model changes. Collateral is common currency across an enterprise and must be properly allocated to wherever it can be used most efficiently. This means that traditional silos – repo, securities lending, OTC derivatives, exchange traded derivatives, treasury and other areas – need to be integrated. Operations groups that have been doing fundamentally the same thing can no longer be isolated from one another; the cost savings that come from process automation and avoiding operational duplication is too compelling.

On the front-office side, changes needed to impact trading behavior, culture and reporting to name a few are often very difficult to implement over a short period of time. Despite similar flows and economic guidelines, different markets and operation centers, even though all under the same roof, traditionally suffer from asymmetric information. To address this challenge a handful of large sell-side players have combined some aspects of these businesses under the “collateral” banner, sometimes along with custody or other related processing business. Others have developed an enterprise solution to inventory and collateral management. We expect that, more and more, management is seeing the common threads and shared risks involved. The merger of business and operations teams translates into a need for technology that can be leveraged across silos.

The business of collateral management is reshaping every process and silo it touches. While the trends we have identified are not brand new, they all stand out for how far and fast they are advancing in 2018 and beyond. Financial services firms that take advantage of these trends concurrently and plan for a future where collateral is integrated across all areas of the business will improve their competitive positioning going forward. To add a sixth trend: firms that ignore broader thinking about collateral management technology do so at their own peril.

This article was originally published on Securities Finance Monitor.

{kind=link}

{kind=link}